Not all Super Funds are the Same…

Is your super what you think it is?

I’ve been having many conversations recently around different types of super funds, retail, industry, and Self Managed Super Funds.

Industry funds are promoting compare the pair, I’m sure you have heard of them or seen them.

Then more recently we’ve had the big banks caught with their hand in the cookie jar, no surprise really.

There’s mass confusion which is the right super fund and do they really have my best interests at heart.

They all have an agenda no matter what fund they are.

Do you really understand your super fund and what it is invested in?

I was researching one recently, an industry fund and was gobsmacked when I noticed that their Balanced option (which most people are invested in) is approx 90% risky investments. How is that Balanced? and that’s where the majority of members are invested.

Now, I don’t know about you, but that’s a hell of a lot of risk to be taking if your 5-10 years out from retirement. That sort of risk is generally more appropriate for someone 20-30yrs out from retirement.

For a lot of my clients who are a long way off retirement, this is still more risk than they are willing to take.

Do you actually know the actual risk you are taking in your super fund?

My role, when advising clients is to not only recommend the best investment strategy based on my client’s individual needs and risk levels but also to advise them the safest path to take. To protect them from what they can’t see.

It’s all well and good while things are going well, another thing when markets correct and all of a sudden you start taking more of an interest in what your super is doing. We never like to lose money, right?

You only have to take yourself back to when the Global Financial Crisis hit, it was a massive shock for most as their investments decreased significantly and all the while you are sitting there wondering why your fund manager or super fund had not reduced their exposure to risky assets. Remember now. It may be a distant memory but it’s worth keeping in mind as there are many lessons to be learned from going through this.

At the time I was working for a business owned by one of the big banks. To be honest there were few solutions for us to react to market movements. It was the old mentality, buy and hold and we’ll see it out.

At the time for most with super, they were selling growth investments to fund their income streams and contributions were invested as they were contributed. Some at stages when it should have been left in cash and for a lot of people they went into the GFC carrying more risks than they were comfortable with.

For me this was not good enough, there was no control at an individual level to reduce risky assets and we didn’t have the information to determine whether markets were expensive or not.

My question was why did we have to hold risky assets when there was little chance of gaining an appropriate return for the level of risk taken.

I felt we did not have enough control over our client’s money but there were very few solutions to fill this void at the time.

So in the last few years, I have been searching for a better way.

Here was my wishlist:-

- My clients must be treated as an individual. To allow for all stages in life and personal preferences.

- My clients had to have total control over the investments in their investment portfolio.

- There was total transparency, they could see all the investments they owned.

- Tax was addressed at an individual level.

- We wanted to move out of the way of bubbles.

- We had flexibility when contributions were invested.

- Our clients had control over what they could control.

- If assets could not provide an appropriate return for the level of risk, they wouldn’t be invested in them.

- The investments were adjusted on a regular basis based on the level of risk the client was comfortable with.

- If investments were looking expensive or overvalued their exposure would be reduced over time and avoided for any new money.

- The clients were communicated on a regular basis and kept up to date with all changes.

As mentioned above a large part of what we do for clients is protect them from the risks they cannot see, prevent them from being blindsided.

I am proud to say I have now been able to introduce an investment solution that addresses all these important factors.

Now, I’m not saying it’s going to guaranteed 100%, but the odds are now stacked in my clients favor. I’d rather be mostly right than mostly wrong while knowing that we’ll avoid most of the carnage when markets correct.

You might be saying but my super fund has performed really well. However you might be missing the critical piece of information, but at what risk level?

We have run the numbers and performance under this investment strategy stacks up with similar returns with less risk taken, now who wouldn’t want that?

It leads to less stress and worry and a much better investment experience especially in a more volatile world.

So, what do I think the problem with the current model is?

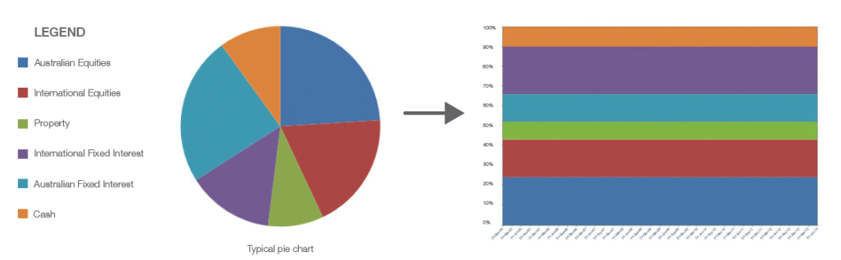

That most super funds are stuck with what we call strategic asset allocation. If you run an SMSF, you would also have an investment strategy that in the majority of cases would reflect this strategy.

Here’s what that looks like:-

Your super fund sets the allocations between risky and defensive assets. At times there are small movements they can make in the ranges but in the majority of cases it is buy and hold and you ride through market cycles.

For me, there had to be a better way.

Here’s what that looks like:-

This is a typical Balanced investment strategy. 50% risky assets, 50% Defensive assets. A true Balanced Fund…

It’s like you are driving down a highway in cruise control on a nice sunny day. You notice a storm approaching ahead. So what do you do? Of course you slow down, your gonna hit the brakes and be cautious. You’re going to wait for the sun to come out before you accelerate again.

So if things are looking a little scary, let’s take some risk off the table, go a little slower or if things look fantastic and we have an open road let’s take a little more risk.

No matter what super fund you are in, it is highly likely your fund will have to remain invested in times of extreme risk, hold risky assets even though they are expensive all the while you are still contributing and investing at extreme levels or into assets that are unlikely to deliver an appropriate return.

I know you are most probably saying that at this stage, well I’ve been getting great returns for years. It’s not now that you are going to be worried, it’s going to be when we go through another market correction and things go bad that you are going to be concerned, concerned you are going to lose money. This is when the panic and worry sets in.

The biggest risk when you are transitioning from employment to retirement is market downturns or corrections. This can put a huge dent in your retirement plans as most experienced around the Global Financial Crisis.

I don’t believe this is good enough anymore.

You deserve better.

I prefer to take a more conservative approach for my clients so they can land there safely at there destination.

Returns are only one metric, here is the only metric you need to focus on. >> CLICK HERE to read more<<

Hope this makes sense and was useful.

This only forms one part of the puzzle when helping people be in more control of their money, there is more to it than just super and an investment strategy but given the conversations I have been having recently, I thought this would be valuable information.

If you haven’t already downloaded our Start Right Guide to Designed Retirement Lifestyles Guide you can download it by clicking here>>

If you have any questions relating to the above feel free to email me at gdoherty@jigsawprivatewealth.com.au

NEXT STEPS:-

Feel like your confused about how to take control of your money, where to start and how to make it work harder for you? Book a 15 min Fast Track call here>>

I have 5 spots left this month…

We’ll get on the phone for a quick chat and:-

- Have a quick look at the issues you are facing or wanting to address and perhaps a couple you don’t know about.

- Help you diagnose what might be getting in the way.

- Give you clarity about the main actions you should be taking now to get you ahead quicker.

Make it a great Life!

Challenging the Status Quo!

Glenn Doherty – CFP – Founder & Financial Organiser at Jigsaw Private Wealth

Website: jigsawprivatewealth.com.au

Email: gdoherty@jigsawprivatewealth.com.au

Mob: 0401 253 729

Request a Retirement Clarity Call

An opportunity to talk through some of your challenges and questions you have around your retirement.

Achieve some clarity and maybe a roadmap on how you can achieve a comfortable retirement.

Schedule hereAdvice Disclaimer: Any reference in this publication to the provision of advice refers to advice of a generic nature, and should not be taken as product or investment recommendations. Before any action is taken based on the information provided, independent financial advice from a licensed financial adviser should be sought. Financial Freedom Project Pty Ltd ATF GA & DC Doherty Family Trust Trading as Jigsaw Private Wealth is a Corporate Authorised Representative of Exelsuper Advice Pty Ltd. The information contained in this publication is of a factual nature only and is not intended to constitute financial product advice. Information is current as at date of publication. This is an online information blog. It does not imply an offering of securities.